In an effort to stay competitive U.S. banks are budgeting big money on tech updates in 2022!

JP Morgan Chase recently announced plans to spend most of its new project budget – a number close to $15 billion – on tech plans as a necessary means to meet customer expectations and compete with other banks and fintechs who are making innovative use of tech.

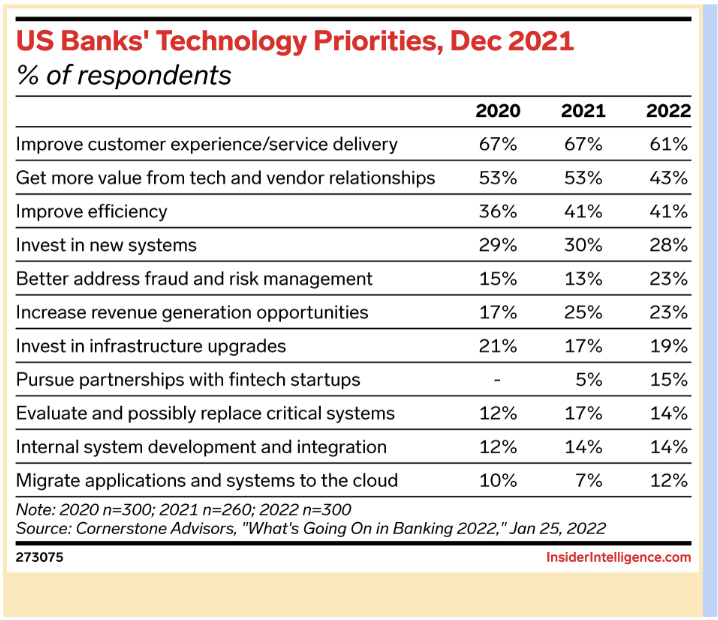

So exactly what type of technology are these dollars being spent on?

Cornerstone Advisors report, “What’s Going on in Banking 2022”, homes in on the key areas where U.S. banks are prioritizing tech spending in 2022:

While there are many areas that banks will focus on in 2022, the biggest increase is in the area of using technology to better address fraud and risk management (jumping from 13% in 2021 to 23% in 2022). This increase in spend, and attention, is not without an inciting statistic: according to the FBI, social engineering/business email compromise scams continue to be the largest source of cybercrime in the country. Yes, larger than ransomware, which grabs all the headlines.

But How? Banks Look to Better Address Fraud and Risk Management

Clay Deutsch, former CEO of Boston Private Bank, and an advisor to PaymentWorks, spelled out the problem banks have this way:

Clay Deutsch, former CEO of Boston Private Bank, and an advisor to PaymentWorks, spelled out the problem banks have this way:

“Every dollar we distribute? We are accountable for knowing the identity [of the recipient] with certainty. Clients don't necessarily like all we have to do for onboarding, validation, identification… and it's a cost problem. Because the solution is just to add people. More pucks are flying at us, so we add more goalies.

If you're a financial institution, this is not just a financial exposure. It's a big regulatory challenge”.

Arriving at the answer of ‘throw more bodies at the problem’ is not unique to banks, to be sure. But the pressure to get it right, might be unique to the banking industry. They have, after all, already solved for protecting check fraud and credit card fraud, however ACH fraud is proving to be a much trickier puzzle to solve. Look at the rest of the priorities on that chart above again. How can they improve the customer experience (don’t lose money to fraudsters!) without disrupting that same experience by adding too much friction? How do you add layers of security and process while also increasing efficiency?

One word: automation.

It’s Half Past Time to Eliminate Manual Vendor Management Processes

Joe Hussey, Vice Chair of Payments at J . P. Morgan, offered this take during our recent live panel discussion with Nacha and J.P. Morgan:

. P. Morgan, offered this take during our recent live panel discussion with Nacha and J.P. Morgan:

“Being automated is the only way you do this. I think there's a stark difference when you say, "I've got a control in place," and it involves fingers and keyboards versus, "I have a systemic way that I know what I'm doing, I know I fully understand step by step," [said otherwise], what control do [you] have in place and is it testable?"

In an earlier blog we published, David Kurrasch, President of Global Payment Advisors, challenged that the only way banks can help their ACH customers is by encouraging them to manage their vendor database with lots of controls. Yes, controls are critical; however, while the banks who are actively prioritizing risk, such as J.P. Morgan and Wells Fargo, offer controls against the bank account itself, these fraud scams typically begin with manual vendor management processes. This is where the organization’s internal controls must step in. But even this is not without risk.

“Every business payments fraud starts the same way: with a change to the vendor master,” said Taylor Nemeth, Head of Payments at PaymentWorks. “If you believe you have a process in place to verify all of these changes, I challenge you to pull the audit log for the past 100 vendor changes. Is your process being followed? Can it be beat? And lastly, exactly how long did all of that work take your staff?”

Hence the 2022 focus by the banks on pursuing efficiency, partnering with FinTechs (like us!), and better addressing fraud and risk management.

Throwing people at the problem, it turns out, is so 2021.

Want to Learn More?